Compared to Brazil, Mexico has a larger unbanked population, with just over 40% of adults with a bank account.

The good news is, that Mexico’s lower house of Congress approved a bill that regulates its fast-growing fintech sector, and it also included crowdfunding and cryptocurrency firms.

As a result, we saw a considerable increase in new FinTechs and more importantly, higher investments in existing FinTechs.

According to Finnovista, Mexico’s fintech landscape is as diverse as Brazil’s, with the payments & remittances sector as the biggest, followed by consumer lending in the number of FinTechs.

Mexico’s challengers and neobanks

Only in 2019, the digital banking sector grew a whoping 200%, the highest growth rate of different fintech sectors in the country, partly due to the number of challengers and neobanks and more customers using these new banking platforms.

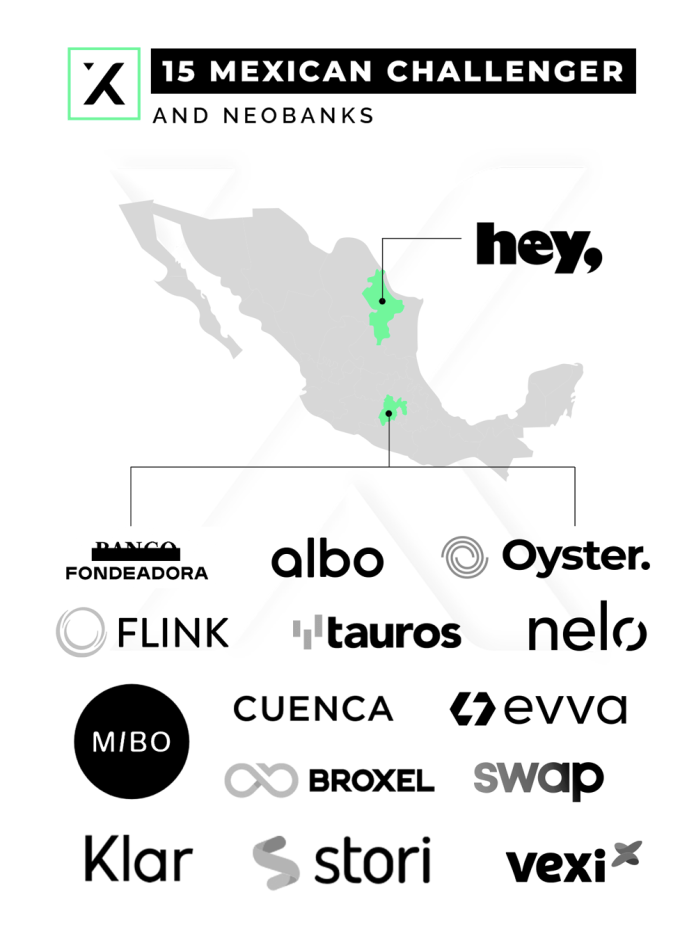

There are around 15 challengers and neobanks, and they are mostly concentrated in the City of Mexico. Despite Mexico being a very large country with geographical diversities, Mexico City has become a real FinTech hub.

And the number keeps growing - just last month, Brazilian challenger Nubank launched in Mexico, rebranded as Nu, and plans to offer a credit card. The company expects that their no-annual fee credit card and hassle-free application process will deliver to Mexicans something that other banks can’t.

Also eyeing Mexico, Spanish neobank Bnext, announced its plans to launch in Mexico, fueled by a fresh new round of €22.5 million. There are rumors that Revolut and N26 are planning to enter the country too.

Fondeadora, which started as a crowdfunding platform has evolved to a challenger bank, announced a US$1.5 million round of investment to become a digital bank, launching a mobile app along with a debit card.

In September 2019, digital banking startup Klar, also known as the ‘Chime of Mexico,’ secured an impressive US$57.5 million in debt and equity seed funding – the largest amount ever raised in a seed round in Mexico.

Albo has secured a US $19 million extension to its Series A financing. They previously raised US $7.4 million at the beginning of 2019, bringing the company’s total Series A funding amount to $26.4 million. Together with Klar, Albo joined the ranks of other Mexican startups that have raised larger-than-average Series A rounds.

Oyster is building a digital banking platform for freelancers, solopreneurs and SMEs, while Stori Card is focusing on the financially underserved population - and it already has 100,000 customers.

Mexican Millennials and Gen Z go digital

Neobank Flink already offers a digital bank account, a card and 120,000 users, they have just launched an additional option on its app for investment in various assets and shares directly through Flink’s platform.

In a recent article, Flink wants to make investors out of millennials. Flink claims is catering for users without large sums to buy expensive stock, especially millennials.

Their USP is to allow users to buy “shares of shares.” For instance, one share of Netflix costs MXN$6,380 (US$340); users can invest as little as MXN$20 (US$1), which is a fraction of a share. Another selling point is that Flink charges no commission or handling fees.

With a focus on Gen Z and Alpha, Mozper is planning to launch its app and debit card for kids and teens. Mozper had a pre-seed investment of US$ 770,000 and is preparing to launch its product in the second quarter of 2020. They are also planning to launch it in Brazil later on.

I had a quick chat with Gabriel Roizner, CEO at Mozper, and Yael Israeli, CFO at Mozper, about Mexican Millennials and Gen Z’ers. They told me that higher socio-economic classes will resemble the global Millennial and Z’er, but lower socio-economic classes have a contrasting reality despite possibly having comparable goals and aspirations to their counterparts.

Israeli mentioned that over 70% of Mexican Millennials show interest in financial culture and education, but the same amount doesn't have a savings account or retirement plan in action. Furthermore, 75% say they have never received any financial education. Mexico is currently further behind in understanding credit, savings and investment.

“Generation Z, and even more so Generation Alpha, some being the children of Millennials, are likely to receive a very different upbringing in regard to their relationship with money, ownership, debt, and savings. This creates an opportunity for socioeconomic advancement.”, Roizner added.

One of the biggest challenges for Mozper is targeting the pre-banked youth (Gen Z and Alpha). This, in itself, is a disruptive form of customer acquisition, before other banks start targeting this generation. But the true challenge will lie in holding onto these customers as they become of age and transitioning into being their primary banking institution as adults. Especially in a market like Mexico where traditional banking is still the gold standard.

Do you want to be the first to read the next weekly overview? Sign up for my Weekly Digital Banking Newsletter here.

Is weekly not enough for you? And do you want to be in the loop with the latest FinTech news every weekday? You should sign up for my Daily FinTech Roundup here

And last but not least: follow me on Twitter or Telegram channel to be the first to hear about any update from the Digital Banking industry!

Las opiniones compartidas y expresadas por los analistas son libres e independientes, y de ellas son responsables sus autores. No reflejan ni comprometen el pensamiento u opinión de Latam Fintech Hub, por lo cual no pueden ser interpretadas como recomendaciones emitidas por la platafomra. Esta plataforma es un espacio abierto para promover la diversidad de puntos de vista sobre el ecosistema Fintech.

Compared to Brazil, Mexico has a larger unbanked population, with just over 40% of adults with a bank account.

The good news is, that Mexico’s lower house of Congress approved a bill that regulates its fast-growing fintech sector, and it also included crowdfunding and cryptocurrency firms.

As a result, we saw a considerable increase in new FinTechs and more importantly, higher investments in existing FinTechs.

According to Finnovista, Mexico’s fintech landscape is as diverse as Brazil’s, with the payments & remittances sector as the biggest, followed by consumer lending in the number of FinTechs.

Mexico’s challengers and neobanks

Only in 2019, the digital banking sector grew a whoping 200%, the highest growth rate of different fintech sectors in the country, partly due to the number of challengers and neobanks and more customers using these new banking platforms.

There are around 15 challengers and neobanks, and they are mostly concentrated in the City of Mexico. Despite Mexico being a very large country with geographical diversities, Mexico City has become a real FinTech hub.

And the number keeps growing - just last month, Brazilian challenger Nubank launched in Mexico, rebranded as Nu, and plans to offer a credit card. The company expects that their no-annual fee credit card and hassle-free application process will deliver to Mexicans something that other banks can’t.

Also eyeing Mexico, Spanish neobank Bnext, announced its plans to launch in Mexico, fueled by a fresh new round of €22.5 million. There are rumors that Revolut and N26 are planning to enter the country too.

Fondeadora, which started as a crowdfunding platform has evolved to a challenger bank, announced a US$1.5 million round of investment to become a digital bank, launching a mobile app along with a debit card.

In September 2019, digital banking startup Klar, also known as the ‘Chime of Mexico,’ secured an impressive US$57.5 million in debt and equity seed funding – the largest amount ever raised in a seed round in Mexico.

Albo has secured a US $19 million extension to its Series A financing. They previously raised US $7.4 million at the beginning of 2019, bringing the company’s total Series A funding amount to $26.4 million. Together with Klar, Albo joined the ranks of other Mexican startups that have raised larger-than-average Series A rounds.

Oyster is building a digital banking platform for freelancers, solopreneurs and SMEs, while Stori Card is focusing on the financially underserved population - and it already has 100,000 customers.

Mexican Millennials and Gen Z go digital

Neobank Flink already offers a digital bank account, a card and 120,000 users, they have just launched an additional option on its app for investment in various assets and shares directly through Flink’s platform.

In a recent article, Flink wants to make investors out of millennials. Flink claims is catering for users without large sums to buy expensive stock, especially millennials.

Their USP is to allow users to buy “shares of shares.” For instance, one share of Netflix costs MXN$6,380 (US$340); users can invest as little as MXN$20 (US$1), which is a fraction of a share. Another selling point is that Flink charges no commission or handling fees.

With a focus on Gen Z and Alpha, Mozper is planning to launch its app and debit card for kids and teens. Mozper had a pre-seed investment of US$ 770,000 and is preparing to launch its product in the second quarter of 2020. They are also planning to launch it in Brazil later on.

I had a quick chat with Gabriel Roizner, CEO at Mozper, and Yael Israeli, CFO at Mozper, about Mexican Millennials and Gen Z’ers. They told me that higher socio-economic classes will resemble the global Millennial and Z’er, but lower socio-economic classes have a contrasting reality despite possibly having comparable goals and aspirations to their counterparts.

Israeli mentioned that over 70% of Mexican Millennials show interest in financial culture and education, but the same amount doesn't have a savings account or retirement plan in action. Furthermore, 75% say they have never received any financial education. Mexico is currently further behind in understanding credit, savings and investment.

“Generation Z, and even more so Generation Alpha, some being the children of Millennials, are likely to receive a very different upbringing in regard to their relationship with money, ownership, debt, and savings. This creates an opportunity for socioeconomic advancement.”, Roizner added.

One of the biggest challenges for Mozper is targeting the pre-banked youth (Gen Z and Alpha). This, in itself, is a disruptive form of customer acquisition, before other banks start targeting this generation. But the true challenge will lie in holding onto these customers as they become of age and transitioning into being their primary banking institution as adults. Especially in a market like Mexico where traditional banking is still the gold standard.

Do you want to be the first to read the next weekly overview? Sign up for my Weekly Digital Banking Newsletter here.

Is weekly not enough for you? And do you want to be in the loop with the latest FinTech news every weekday? You should sign up for my Daily FinTech Roundup here

And last but not least: follow me on Twitter or Telegram channel to be the first to hear about any update from the Digital Banking industry!

Las opiniones compartidas y expresadas por los analistas son libres e independientes, y solamente sus autores son responsables de ellas. No reflejan ni comprometen el pensamiento o la opinión del equipo de Latam Fintech Hub y, por lo tanto, no pueden interpretarse como recomendaciones emitidas por la plataforma. Esta plataforma es un espacio abierto para promover la diversidad de puntos de vista en el ecosistema Fintech.

Este contenido es solo para usuarios Prime 👑 del Hub.